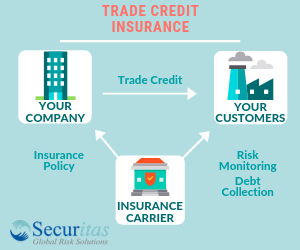

Trade Credit Insurance, sometimes called Accounts Receivable Insurance, is a method of protecting a company’s accounts receivable against the risk that one or more key customers will fail to pay for goods and services. This type of insurance covers the risk of unpaid invoices that may arise as a result of protracted default, insolvency, or bankruptcy of a customer (also known as a buyer). Trade credit insurance protects your cash flow and covers your business with your customers so that when they fail to pay you or go under, your company still gets paid.

What are the Reasons to Invest in Trade Credit Insurance?

A credit insurance policy can do more for a company than just protecting accounts receivable.

Large companies, and especially multinational entities, invest in trade credit, business credit, or export credit insurance for a variety of reasons, including:

1. Increased Sales and Expansion: When a company’s receivables are insured, they can safely sell more to existing customers, as well as expand into areas that would otherwise be too risky.

2. Improve Cash Flow: a credit insurance policy can improve your cash flow by reducing the number of days a sale can be outstanding. It also allows for the outsourcing of debt collection services at no extra cost.

3. Better Financing Rates from Your Lender: Lenders look favorably on companies that have taken the added measure of protection that trade credit insurance offers. They will typically lend more capital for insured receivables and may reduce the cost of funds.

4. Reduce Reserves of Bad-Debt: Insuring a company’s accounts receivable can free up capital that would have originally been set aside in case the customer failed to pay. This means more liquid cash flow available for business initiatives.

5. The Protection Pays Off: Credit insurance policies may offset its own cost due to the way in which it allows a company to increase sales and profits without additional risk. In addition, credit insurance premiums are tax deductible.

The credit insurance premium is calculated by using a percentage of your turnover combined with level of risk. In other words, the number depends on who you are selling to, how much coverage your company needs for each customer, customer ratings, loss history, and the business sector.

On average, a trade credit insurance premium will be a fraction of one percent of company sales. The rate can be lower or higher depending on the variables listed above.

What Do I Need to Know About Policy Coverage?

Policies are written on an annual basis and can cover risks that are commercial or political. Once the policy is set, the credit insurer will assign the policyholder’s insured customers a specific credit limit, which is the amount covered if a buyer fails to pay.

Unlike other types of insurance, a trade credit insurance policy does not get filed away for renewal next year, it is a dynamic relationship. This type of policy can continue to change over the course of the year and the credit manager will play an active role in this process.

New buyers and additional coverage can be requested if needed. In this case, the insurance company will determine whether to approve the coverage by investigating the risk.

The insurer will continue to monitor your buyers and their creditworthiness. Companies we work with such as Atradius, Euler Hermes, and Coface will gather information about your customers by a variety of methods such as public records, receipt of financial statements, and information that is obtained through other policyholders that sell to the same buyer. This will be of great value to your company because the information you can access through the insurers database will help you make smarter business decisions.

Should you need to file a claim, our team of claims professionals will guide you through the process.

In a way, your credit insurer becomes an extension of your team. For example, if the records in the insurance carrier’s database suggest that your buyer is experiencing financial trouble, all policyholders that sell to that particular buyer will be alerted so that a plan can be set in place to avoid any losses before a claim is even filed.

How Do I Know Which Insurance Carrier to Choose?

There are many insurance carriers that offer trade credit insurance and each of them may differ in the amount that they decide to cover for your buyers, as well as their terms and conditions. Having a deep understanding of each of these differences will help you decide the best option for your company.

A trade credit insurance broker is invaluable in this process. Kirk Elken and Peter Seneca have over 35 years in the area of trade credit insurance. At Securitas Global Risk Solutions, we work for your company’s business interests, not the insurance carrier’s.

First, we work to understand your business needs and financial goals, key buyers, and credit exposures. Then, we send your policy application to multiple insurance carriers for quotes, which include buyer coverage commitments and proposed terms and conditions.

Next, we schedule a meeting to review the results. Using our knowledge of the insurance carriers, we can advise you on which policy will be best suited for you in terms of premium price, coverage, and advantages or disadvantages of working with each carrier.

After working together to elect the best policy at the most competitive price, we continue to work with and negotiate with the insurance carriers as your needs evolve.

Does it Cost More to Use a Trade Credit Insurance Broker?

There is no additional cost to you for using a trade credit insurance broker. This means that on a given insurance policy, your rate will be the same whether you decide to undertake the process alone by going directly to an insurance carrier or work with a trade credit insurance broker.

In fact, you are likely going to pay less on your premium because you have your choice of multiple carriers, rather than being locked into one.

In Summary

Trade credit insurance is different than traditional insurance. It covers accounts receivable so that you can protect your company against buyer insolvency, slow-pay, and bad debt. In addition, a trade credit insurance policy is a partnership with the insurance carrier that can provide their database information and knowledge to improve your trade decisions. Companies can also benefit from trade credit insurance through its ability to affect your sales expansion to new and existing buyers.

Navigating the world of credit insurance and the insurance claims process can be complicated and challenging. Using a broker like Securitas Global Risk Solutions gives the balance of power back to the client in the form of our knowledge of the industry, our understanding of your company, and our ability to provide you the carrier that offers the best coverage at the lowest rate.

As an insurance broker rather than an insurance agent, Securitas Global Risk Solutions is able to apply to multiple carriers to find the best contract, with the most coverage, for the least cost. A carrier’s agent can only advise you as to that carrier’s specific contract. We have a team of experts who are available to you 24/7 to answer any questions or concerns. Additionally, our service comes at no charge to you.

On May 8, the U.S. Senate formally confirmed three of the Trump administration’s nominees to the board of directors of the Export-Import Bank of the United States (EXIM). The nominees include Kimberly A. Reed, confirmed as president and chairman of the board, Spencer T. Bachus III, and Judith DelZoppo Pryor. Two additional nominees remain under consideration by the Senate.

The confirmation establishes a quorum of three members on the EXIM board of directors need for the bank to authorize transactions greater than $10 million. EXIM had been operating since July 2015 without a full quorum and was limited in its ability to approve larger, typically long-term financing deals.

EXIM’s inability to fully conduct larger deals hindered its overall ability to support smaller transactions that typically assist small and medium-sized enterprises (SMEs) and to be self-funding—covering its operations on fees and interest it receives from its beneficiary clients. In fiscal year 2018, EXIM reported $3.4 billion in transactions, down significantly from a high of $35.8 billion in 2015, and also forecast a $492.2 million operating deficit. The Wall Street Journal reports that EXIM’s own internal estimates value the amount of lost transactions since mid-2015 at $21.5 billion. While the restoration of EXIMs full financing capacity is welcome news to businesses seeking to increase American exports, EXIMs legal authorization will lapse on September 30, 2019 if Congress fails to reauthorize it past that date.

The Ex-Im Bank helps support U.S. exports through a range of programs, including guaranteeing loans to foreign buyers, credit insurance and some direct lending to foreign companies. To learn more about the range of products offered by the EXIM Bank, click here.

As a certified EXIM broker, Securitas has years of experience working with U.S. companies seeking to access EXIM’s services to help generate export-driven growth. Offering services such as trade credit insurance and risk insurance, Securitas is able to provide these trade insurance solutions, often at no cost to the exporter, and then works with its customers structure insurance solutions that meet their goals of sustained and secure long-term growth. In 2015, Securitas was named EXIM Broker of The Year.

Securitas is ready to help businesses, particularly SMEs interested in pursuing an export strategy, learn how to access EXIM’s services.

As an insurance broker rather than an insurance agent, Securitas Global Risk Solutions is able to apply to multiple carriers to find the best contract, with the most coverage, for the least cost. A carrier’s agent can only advise you as to that carrier’s specific contract. We have a team of experts who are available to you 24/7 to answer any questions or concerns. Additionally, our service comes at no charge to you.

Risk management often requires a counter-intuitive approach, challenging ourselves to think through whether we have accurately assessed the possible risks that face our businesses. Planning for a range of outcomes requires an evaluation of downside risk. This runs counter to the optimistic view we naturally have for our efforts in building individual enterprises. Yet the recent bankruptcy of Toys-R-Us highlights why, even when times are good and indicators seem positive, “black swan” events can happen. The time to plan for those events is ahead of the crisis.

Imagine the scenario: It is August 2017. As the CEO of a toy manufacturing company, your firm is coming up on the biggest, most lucrative season of the year – the December holidays. Irrespective of tradition, the bringer of gifts will need some 21st century manufacturing support — your toy company is just the one for the job!

Knowing the retail toy sector is largely seasonal, your company team understands the traditionally longer manufacturing lead times needed to stock store shelves. They have worked hard, marketed and won contracts from the major toy retailers in advance of the big season. Your company also anticipated the early holiday shoppers and made sure products will be delivered by the middle of September. It is this holiday-season Accounts Receivable that will fund your firm’s working capital throughout a good portion of next year.

Now ask the question: Do you need trade credit insurance on those Accounts Receivable? Is it a luxury or a necessity? There is market concentration with a historically large buyer that could not possibly file for bankruptcy right before the holiday season, the best time of the year. You decide to gamble with that thought in mind.

Your CFO, however, has been reading the trade press on the difficulties facing the retail sector, as the major box stores wither under cost competition from online retailers. She recommends you take a look at insuring buyer risk, just in case retailing has indeed crossed a Rubicon and become an online enterprise. The is not really the news you want to hear going into the busiest season of the year — but then again, you made her CFO because she is willing to bring you the hard news. With a quick call to your broker, you are able to line up a trade credit solution covering the risk concentration associated with a large buyer. As it turns out, this one call can be the move that saves your toy company. Unlike many of your competitors, you will now get paid for the shipped merchandise.

When everything is going well, accounts receivable are being paid and aging accounts are small, trade credit insurance might look like a luxury. However, it is also a good time to review your options and risks with an experienced trade credit insurance expert at Securitas Global. The premium rates can be lower with greater underwriting capacity. Even more importantly, markets recognize the value of supporting existing clients on credits like Toys “R” Us. Just prior to the bankruptcy filing, our Securitas Global team heard comments from vendors with respect to getting trade credit insurance on Toys-R-Us that included: “It’s expensive” and “We’re concerned, but we don’t think they’ll file yet.” When it became clear there would be a loss, and insurance was no longer available since underwriters will not insure a certain loss, the cost of protection became secondary. The conversation became one of whether any available coverage options existed.

The moral of the story: The time to put trade credit insurance in place is before there is a known risk. As one client shared “I have too much invested in my business to risk it because one of my customers can’t pay me.” Securitas Global can develop a customized solution to cover your needs at the right price point. We work with clients to determine their level of risk and how to allocate it then devise a policy that will cover their specific needs. This can include coverage for overseas buyers and ways to mitigate political risk. By insuring accounts receivable, we are able to preserve your firm’s working capital and support credit access.

The Export-Import Bank of the United States (EXIM) is the official export credit agency of the United States. Its mission is to support American jobs by facilitating the export of U.S. goods and services. It does so by assuming credit risk, primarily through two programs – extending export credit insurance for exporters and providing working capital guarantees. These programs are available to companies of any size with 80% of authorizations are to SBA defined small business.

The Current State:

EXIM is congressionally authorized through 2019. While this seems several years from now, it’s important to note the last two authorizations have been tenuous, including a period in 2015 when its charter lapsed for six months. President Obama and congressional Democrats generally supported EXIM through this period, however there was an influential group of House Republicans that held up authorization process.

In addition to upcoming the re-authorization debate, EXIM also lacks three board members. Therefore, it does not have the quorum required to approve authorizations over $10MM.

The new administration brings renewed and increased speculation regarding the future of EXIM. President Trump campaigned on a platform of reduced government and seemed less friendly toward global trade. However, he heavily emphasized his business background and experience, which included strong support of U.S. manufacturers and small businesses, both of which he believes are critical to economic growth.

Against this backdrop, members of the Securitas team attended the EXIM 2017 Annual Conference on April 7-8 to learn more about the bank’s future.

Key Takeaways:

95% of global population and 80% of global GDP is outside the U.S.

According to the Organization for Economic Co-operation and Development (OECD), there are 32 countries with Export Credit Agencies (ECAs) that compete with the U.S.

Exports will become even more critical in helping the U.S. grow its GDP, reduce the debt and balance the budget.

In order to compete globally against China, the U.S. needs to increase its support of exports. For example, the U.S. EXIM Bank supported $10 billion in authorizations in 2015. In comparison, China supported $500+ billion in exports through EXIM-China, China Development Bank and Sinosure).

Jobs created by export-related business tend to pay an estimated 18% more according to the International Trade Administration.

During a panel discussion regarding the future of EXIM, congressional members Jack Ryan, R-PA and Chris Collins R-NY both indicated President Trump fully supported the bank and recognized the need to support U.S. exporters though tax policy and regulation reform. They further indicated his commitment to a fully functioning bank by filling the vacancies on its board with immediate appointment approval of three new board members.

While there is still internal debate within the Republican caucus regarding the future of EXIM, it does appear the agency has the backing of President Trump and will continue to be an important tool in the U.S. government’s toolbox to support exports.

Get Your Free Guide to Trade Credit Insurance

Get Your Free Guide to Trade Credit Insurance Get Your Free Guide to Trade Credit Insurance

Get Your Free Guide to Trade Credit Insurance