Carlyle Aviation Partners' lawsuit against insurers The lawsuit was filed on October 31 against over 30 insurers in...

Climate Change and its Impact on Country Risk

Used with Permission from Atradius.us

Climate change raises country risk, but offers business opportunities as well.

Summary

-

-

- Climate change has a negative impact on economies worldwide, their public finances and international trade. The consequences of climate change thus raise the country risk related to export transactions and international contracting.

- Changing rainfall patterns, sea level rise and natural disasters mainly affect countries in Africa, the Caribbean and the Asia-Pacific region. These countries often combine a high vulnerability to climate change with a poor readiness to respond to the consequences of it.

- Internationally operating companies develop technologies and build infrastructure that are used for the climate adaptation initiatives of the countries affected. In this way they make a positive contribution in the battle against climate change.

-

In a period when the Covid-19 pandemic swept the planet like a shockwave, scientists and policymakers kept that other big problem, climate change, on their radar. Fortunately they did, because – just like the pandemic – global warming is a major threat to humanity and action is urgently needed. But there is a second parallel. Like Covid-19, climate change not only causes personal suffering, it also involves great financial and economic damage. Increasing drought, sea level rise and natural disasters affect the incomes of individual citizens and businesses and represent high costs for governments. Or, as the IMF points out in a recent background paper, “climate change redistributes income and affects asset valuations, with repercussions for public and private sector balance sheets, financial flows and financial stability, trade, and exchange rates”. As a result, climate change affects the country risk related to foreign trade and projects in countries around the world in several ways.

Meanwhile, climate change also offers opportunities. Development of new technologies and investments in, for example, irrigation, desalination plants and the energy transition have a positive impact on economic growth and create new jobs.

In this Research Note, we first pay attention to the most prominent consequences of climate change for individual countries: changing precipitation patterns, sea level rise and the climate change-related increase of natural disasters in coastal areas. The focus will be on the countries which feel the impact the most: emerging economies in Africa, Latin America and the Asia-Pacific region. Using the ND-GAIN index for climate change, we identify which countries are doing poor regarding their vulnerability and readiness for these various kinds of impact.

Fortunately, there is a bright side of climate change as well. In the last section of this note we mention a series of projects that show how internationally operating companies are involved in the fight against and adaptation to climate change.

The ND-GAIN index: mapping the vulnerability and readiness of countries for climate change

A useful methodology for mapping the consequences of climate change for country risk is provided by the Notre Dame Global Adaptation Initiative (ND-GAIN). This group of scientists from various disciplines, affiliated with the University of Notre Dame (Indiana, USA), publishes the ND-GAIN Index for 181 countries annually, with sub-indices for both countries’ vulnerability and the degree to which they are ready to effectively use investments to respond to the consequences of climate change (their ‘readiness’). The underlying data and country rankings are used by private companies as well as non-governmental organizations and governments in making decisions related to production, investments, policy choices and communication.

The ND-GAIN index measures the first component, vulnerability to climate change, by including the consequences for food supply, access to water, health, the ecosystem, the living environment and infrastructure, whereby for each of these six components six indicators are included. Examples of these 36 indicators are the expected impact on agricultural crops, dependence on natural resources, the expected increase in floods and the impact of sea level rise. The second component, readiness, is measured against a total of nine economic, political/administrative and social indicators. Examples are the business climate, political stability and the quality of the ICT infrastructure in the country concerned.

Changing rainfall patterns: major threat to agriculture-intensive Africa

Higher temperatures and the changing rainfall patterns make it such that relatively dry countries become even drier and wet countries wetter. Prolonged drought can occur anywhere in the world, but some regions and countries are more severely affected than others. Vulnerability to drought is exacerbated, among other things, by poverty and incorrect use of land. It is therefore no surprise that African countries are the most vulnerable. Most of these countries are located in Southern and Central Africa, some others in Asia (India and Nepal).

In 2019, the impact of climate change was clearly visible when southern Africa was hit by extreme drought. But too much rain can be a problem as well. In the Horn of Africa, weather conditions changed from an extreme drought in 2018 to heavy rainfall in 2019, resulting in floods and landslides. In East Africa, heavy rainfall contributed to strong crop growth, but also brought a severe locust plague.

Higher temperatures and heavy rainfall threaten public health

Due to the temperature rise in the coming years and the more frequent change in precipitation patterns, extreme weather events will occur more often. These consequences of climate change will have a negative impact on public health, agriculture and energy supply. With regard to public health, African countries in particular are vulnerable. A rise in temperature and heavy rainfall make the living environment suitable for insects that transmit diseases such as malaria and dengue fever.

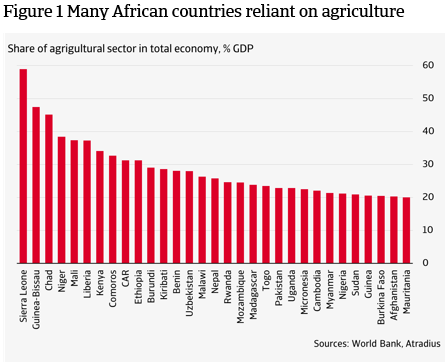

Agriculture is the sector most vulnerable to a rise in temperature and changed precipitation patterns. Risks include a decrease in production, an increase in pests and diseases and floods that affect infrastructure. The figure below shows all countries in the world where the agricultural sector as a percentage of GDP represents 20% or more. It clearly shows that mainly African countries are exposed to outsized agricultural sectors. In many of them, it concerns mainly subsistence agriculture.

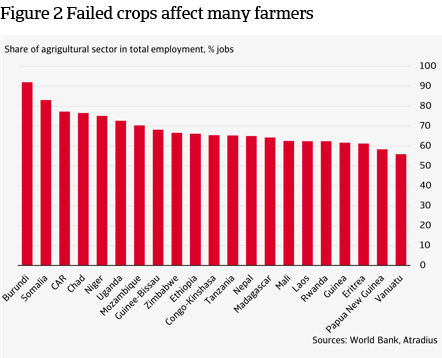

In many countries, the agricultural sector creates the most jobs. The figure below shows the countries where the agricultural sector has a share of 50% or more in total employment.

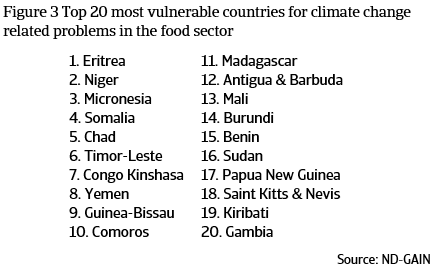

Failed crops increase food insecurity and deteriorate living standards in many countries. The ND-GAIN index also includes a so-called food score. It measures the vulnerability of a country to climate change in terms of, among other things, food production and demand for food. Indicators that are considered include the expected change in grain yields, expected population growth, dependence on food imports, population in rural areas and agricultural capacity. Figure 3 shows the countries that emerge as most vulnerable from this food index.

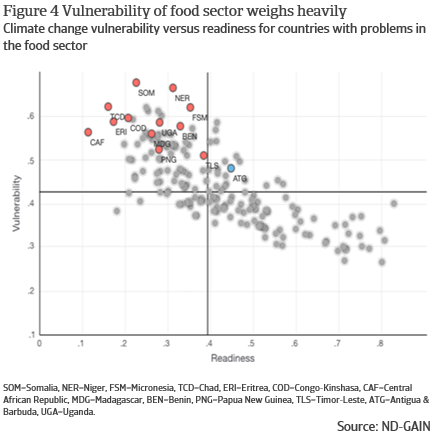

Figure 4 presents a matrix of the countries’ ND-GAIN scores for both their vulnerability and their readiness. Almost all of the most vulnerable countries listed in figure 3 are in the top left quadrant. This means that these countries are vulnerable and have taken few measures to adapt to climate change. Somalia (SOM) and Niger (NER) are in the weakest position. Antigua & Barbuda (ATG, in blue) has a poor score for the food sub-index and is also relatively vulnerable to climate change, but the country has already taken steps to address the consequences, bringing it in the top right quadrant.

Faulty energy supply

Drought can also have a negative impact on energy supply if hydropower is an important source in a country’s energy mix. In 2019, drought seriously disrupted the energy supply in Zambia and South Africa, with a significant impact on the economy as well. Countries where hydropower has a large share in the energy supply are mainly located in Latin America. BP data shows that in Latin America around a quarter of the energy supply is generated by hydropower in Ecuador, Brazil, Venezuela and Peru. There are also some countries in Asia where hydropower takes up a large part of the energy supply, such as Vietnam and Sri Lanka where hydropower accounts for 14% and 12% respectively of total energy consumption. For Africa, the International Energy Agency states that hydropower accounts for about 17% of the continent’s electricity supply on average. Countries where hydropower provides more than 80% of electricity are Congo-Kinshasa, Ethiopia, Malawi, Mozambique, Uganda and Zambia.

Since Africa is very vulnerable to climate change, the energy supply is most exposed. Forecasts indicate that southern Africa will be facing more droughts, while East Africa will have more rainfall. As a result, hydropower capacity is expected to decline in Congo-Kinshasa, Mozambique, Zimbabwe, Zambia and Morocco. An increase is foreseen in Egypt, Sudan and Kenya.

Support for adaptation measures

Low-income countries are most vulnerable to climate change. These countries lack the financial resources and technology to increase their resilience and adapt to changing weather conditions. That is why these countries are receiving support from various organisations. For example, the World Bank helps countries to adapt to climate change with investments and technological assistance. To this end, it has set up the Adaptation and Resilience Action Plan. With regard to agriculture, its aim is to increase the resilience of farmers and support them with climate-smart solutions. For example, the development of climate-smart agriculture involves improved seeds and diversification of food production. Improved agricultural technology also includes manure, tractors and irrigation systems.

Sea level rise: huge problem in Asia-Pacific and the Caribbean

One of the most obvious consequences of climate change is sea level rise. As global average temperatures increase, polar ice caps in Greenland and Antarctica, sea ice in the polar regions and glaciers and snow in high-altitude parts of the world are melting, causing sea levels to rise. Another factor is that warmer water has a greater volume than cold water. Estimates of sea level rise to the end of the century range from 60 to 220 centimetres, depending on the extent to which humanity will succeed in reducing CO2 emissions. At first sight, this increase may still seem limited, but it has major consequences. According to calculations by American research group Climate Central, by 2050 the habitat of no less than 300 million people is at risk of being flooded once a year on average. At the end of the century, the habitat of 200 million people would be permanently below sea level, depending on coastal defences being built or population relocations. For many of the approximately 110 million people who already live in areas below sea level, the authorities will have to take measures to keep them safe as well.

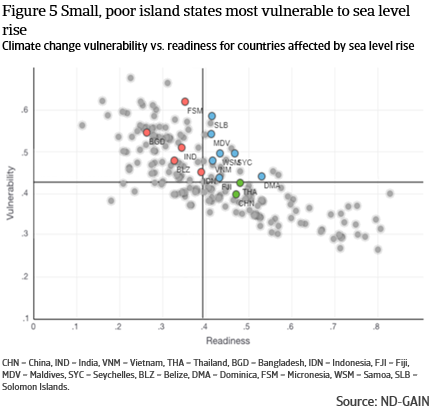

The threat posed by sea level rise is especially relevant in Asia, the Pacific and the Caribbean. This is of course largely related to the elevation of the coastal areas, but also the height and quality of the coastal reinforcement present. Research using a so-called Digital Elevation Model supplemented with machine learning techniques shows that the coastal areas of China, Bangladesh, India, Vietnam, Indonesia and Thailand together account for about 75% of the aforementioned 300 million people whose habitat is endangered within 30 years.

Whereas for large countries in Asia it often concerns limited parts of the country, in the island states in the Pacific and the Indian Ocean most of the area is often threatened by the rising sea levels. For example, three-quarters of the population of the Marshall Islands lives in threatened areas, in the Maldives about one-third. In this sense, a large size of a country or economy is a mitigating factor for sea level rise, as only part of the country is affected.

The small island states in the Pacific and the Caribbean generally have limited administrative and technical capacities and limited financial resources. However, there are differences. For example, the Maldives, a country with a relatively high GDP per capita, can be found in the quadrant with vulnerable countries that are more than average ready for the consequences of climate change. In order to guarantee the high income from tourism, the government has invested heavily in coastal reinforcement and land reclamation.

Small island states dependent on foreign funding

Fiji is also on the right side of the vertical median, while still being financially vulnerable. For example, the World Bank has calculated that the country will still have to invest approximately 100% of its GDP in the coming ten years to prepare the country for the expected sea level rise and the increase in natural disasters. Fiji, like other island states in the Pacific and the Comoros (off the east coast of Africa), is mainly dependent on foreign funding. Support is coming from the IMF and World Bank, neighbouring countries such as Australia and New Zealand, or from countries that provide aid or provide loans for political-strategic reasons. For example, the IMF supported the Comoros after a cyclone disaster with ample emergency aid, Micronesia receives aid from the US to build a buffer for the future (with limited success) and Samoa receives loans from China. The Solomon Islands have exchanged a long-term relationship with Taiwan for a financially more favourable relationship with China.

Increasing natural disasters in coastal areas

The countries vulnerable to sea level rise are often also affected by increasing natural disasters, such as severe storms and hurricanes. As of now, there is no scientific consensus on a direct link between climate change and hurricanes, but in recent decades natural disasters in coastal areas have been increasing. A causal relationship can be explained by the fact that a warmer atmosphere heats the surface water at sea, which in turn increases the severity of hurricanes. Since the early 1970s, the number of hurricanes in the heaviest categories has nearly doubled worldwide, while the durations of the hurricanes and also the highest wind speeds have increased by almost 50%.

Natural disasters have a major impact. For example, in 2019 alone, natural disasters caused 11,755 deaths worldwide, while 95 million people were affected. Some of this is not related to climate change (such as earthquakes, while even without climate change there would be hurricanes), but the fact that floods were responsible for 43.5% of the number of deaths, extremely high temperatures for 25% and storms for 21.5%, makes it plausible that climate change did play a major role. Storms and floods were responsible for 68% of the deaths. The World Bank reports that 75% of the damage caused by natural disasters since 1980 has been attributable to extreme weather events and that climate change threatens to push some 100 million people into extreme poverty over the next ten years.

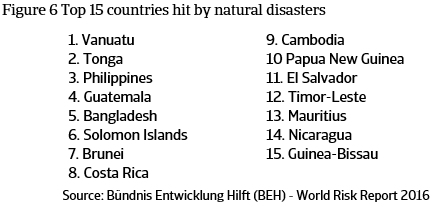

The differences per region and per country are large, but here too the poorer countries are generally hit harder than the high-income countries. According to the World Bank, low- and middle-income countries experienced 32% of storms in the period 1998-2018, but 91% of the storm-related fatalities. On the list of countries most affected by natural disasters published by the United Nations University Institute for Environment and Human Security (UNU-EHS), countries in Asia and the Pacific again dominate, alongside countries in Central America and the Caribbean in particular.

The impact of severe natural disasters is often relatively large for small island states, just as with the threat of sea level rise, and is therefore an important factor in determining the level of country risk. For several of the island states, ND-GAIN does not give a vulnerability score and therefore no ND-GAIN overall score. However, looking at only the readiness score of ND-GAIN for countries that have to deal with natural disasters (and which therefore also takes into account the extent to which these countries deal with other consequences of climate change), we can conclude that the picture is diverse. Mauritius, Brunei and Costa Rica score relatively well in this respect, while Guinea-Bissau, Bangladesh, Papua New Guinea, Nicaragua, Cambodia and Guatemala score poorly in terms of ‘readiness’. Large countries that combine a relatively high risk of natural disasters with a poor readiness score are (again) Bangladesh and, to a lesser extent, the Philippines and several Latin American countries.

The bright side of climate change: business opportunities

Many emerging economies are vulnerable to one or more elements of climate change. Heat, drought and changing rainfall patterns are a major threat to agriculture-intensive Africa. Sea level rise and increasing natural disasters in coastal areas create problems in Asia, the Pacific and the Caribbean. Though some countries are lagging, many of them, often helped by multilateral or bilateral partners, take measures for both the short and long term, thereby creating business opportunities.

In fact, this applies to all channels through which climate change affects country risk. Businesses active in the development of new technologies for and construction of irrigation and desalination plants have a large playing field in Africa. Meanwhile, the great untapped potential of renewable energy in Africa offers opportunities. The French company Mascara Renewable Water for example has partnered with a local company to build a solar-powered desalination plant in South Africa which will convert sea water into fresh water. Netherlands-based Independent Energy B.V. exports to countries across Africa, the Middle East and South America, where there is interest in solar energy systems, but a serious lack of knowledge about how to build them properly.

On a much bigger scale are the opportunities created for construction and maritime companies active in the construction of offshore wind farms. Taiwan, for example, has contracted Siemens Gamesa, a leading supplier of wind power solutions, the Denmark-based multinational renewable energy company, Ørsted, and Dutch companies like Heerema Marine Contractors, Van Oord Offshore and Boskalis Westminster Dredging to be part in large offshore wind projects.

Countries affected by sea level rise and natural disasters in Asia and the Caribbean are in need of expertise when it comes to coastal defense and water management. Kiribati, the extensive island state in the Pacific, will seek support from China and other allies to elevate islands from the sea, partly through dredging. The Maldives, in the Indian Ocean, combine coastal defense and land reclamation with the development of a port and other improvements of the infrastructure, creating various opportunities for Indian and other foreign companies.

Climate change in the first place is a threat for most countries in the world, and especially the less wealthy ones in Africa, Latin America and the Asia-Pacific region. Internationally operating companies can benefit from the opportunities climate change creates and, meanwhile, make a positive contribution to the climate adaptation initiatives of these countries.

Used with Permission from Atradius.us

Since 2004, Securitas Global Risk Solutions (“Securitas”) has helped clients worldwide develop credit and political risk transfer solutions that provides value on numerous levels. As an independent trade credit and political risk insurance brokerage, Securitas is focused on developing comprehensive solutions that meet the needs of clients, ensuring complete understanding of policy wording and delivering excellent responsive service.

Recommended News

Aircraft Lessors Sue Insurance Companies for Coverage in Russian Confiscation Debacle

The Sudden Bankruptcy Filing of Vital Pharmaceuticals Inc / Bang Energy

Could a Large Manufacturer be a Credit Risk? Vital Pharmaceuticals is the third largest energy drink manufacturer in...

Major Country Risk Developments

Posted with permission from greatamericaninsurancegroup.com Overview The global economy has suffered four shocks...